Oil prices rose only modestly last week after fresh setbacks in US-Iran negotiations, a notably muted reaction compared to similar developments in recent weeks.

According to Commerzbank AG, this tempered response reflects the market’s improved ability to absorb disruptions through inventory draws, rerouting, and demand adjustments.

Muted price reaction to geopolitical risks

As hopes for a swift US-Iran agreement faded once again, Brent crude and European natural gas saw only slight gains last week.

However, the increase in oil prices was far more restrained than in previous episodes of heightened tensions.

Norman Liebke, FX and commodity analyst at Commerzbank AG, explained the dynamics:

“This can likely be explained by the fact that oil inventories are lasting longer than expected, even though inventories of some oil products have already fallen significantly.”

He noted that the supply-demand gap caused by the Strait of Hormuz closure has been partly bridged not just by inventory draws but also through rerouting of exports, lower demand in some regions, and strategic releases of reserves.

However, oil prices have risen more than 4% on Monday as geopolitical tensions simmered amid Israel’s latest attacks on Lebanon.

Markets remain uncertain and increasingly sensitive to geopolitical headlines.

Inventory buffer provides breathing room

This resilience in inventories has given the market more room to absorb shocks than many had anticipated.

While product inventories (particularly gasoline and distillates) have declined noticeably, overall crude stockpiles have held up better, preventing a sharper spike in prices despite ongoing geopolitical uncertainty.

The situation remains fluid, however. Any prolonged closure of the Strait of Hormuz or escalation in the conflict could still test these buffers in the coming months, especially as the Northern Hemisphere enters peak summer demand season.

Key reports to shape market direction this week

This week will bring several important data releases that could set the tone for oil markets through the rest of 2026 and into 2027.

The US Energy Information Administration (EIA) is scheduled to publish its monthly Short-Term Energy Outlook (STEO), which includes updated forecasts for global supply and demand.

Liebke highlighted the significance of recent production data:

“Most recently, it reported a decline in daily global oil production of approximately 10.5 million barrels per day for March and April. This decline is likely to have intensified further in May.”

He added that this production drop is of limited relevance to the global market for now because the oil cannot be shipped due to the Hormuz blockade.

The EIA will also address US LNG export capacity, a critical topic given constraints on Qatari LNG.

The STEO report also discusses US LNG export capacity. This is particularly interesting because Qatari LNG supply will be curtailed by up to 20% over the next three to five years due to damage at the world’s largest LNG terminal.

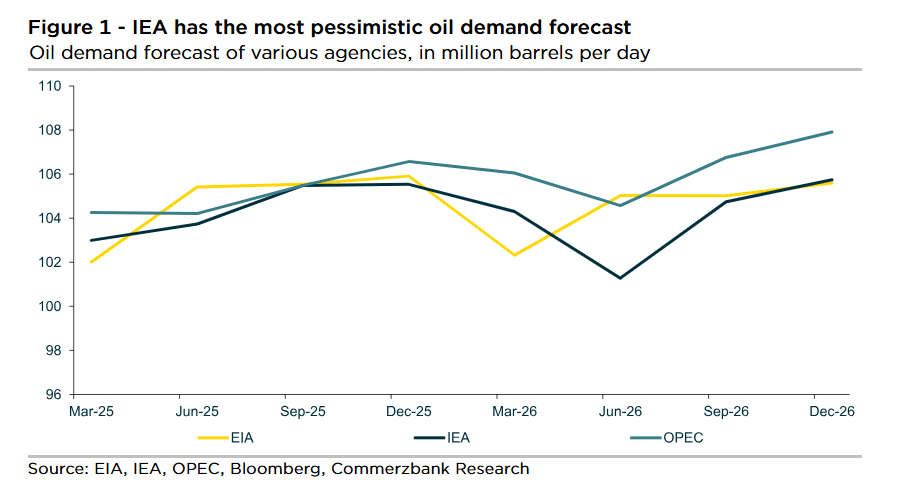

OPEC and China data in focus

On Thursday, OPEC will release its monthly report.

The cartel’s Secretary-General recently indicated that OPEC would maintain its relatively optimistic demand forecast, standing in contrast to more cautious projections from the IEA and EIA.

Chinese foreign trade data, due next week, will also be closely watched. Liebke pointed out.

China’s crude oil imports by sea, which have fallen to a ten-year low, are likely to have reduced competition in Asia for available oil. Should customs data show a decline in crude oil imports in May — which is to be expected — this alone is likely to put downward pressure on prices.

The current environment highlights the oil market’s evolving ability to adapt to geopolitical shocks.

While inventories have provided more support than expected, the combination of seasonal demand strength, potential further production curtailments, and ongoing uncertainty around the Strait of Hormuz suggests that volatility is likely to persist.

Market sensitive

Liebke and other analysts believe the market remains sensitive to both positive diplomatic developments and any signs of renewed escalation.

The upcoming EIA, OPEC, and Chinese data releases will be crucial in determining whether the current resilience holds or if renewed price pressure emerges.

For now, the oil market appears to be in a cautious holding pattern, balancing geopolitical risks against physical market realities that have proven more accommodating than many feared.

How this week’s reports shape expectations could determine whether this resilience continues or gives way to sharper price movements in the second half of 2026.

The post Oil market faces key test as inventories buffer geopolitical risks appeared first on Invezz